Depositing business transactions into a personal account can lead to several legal and financial consequences, including fines and penalties. Here are some potential issues you could face:

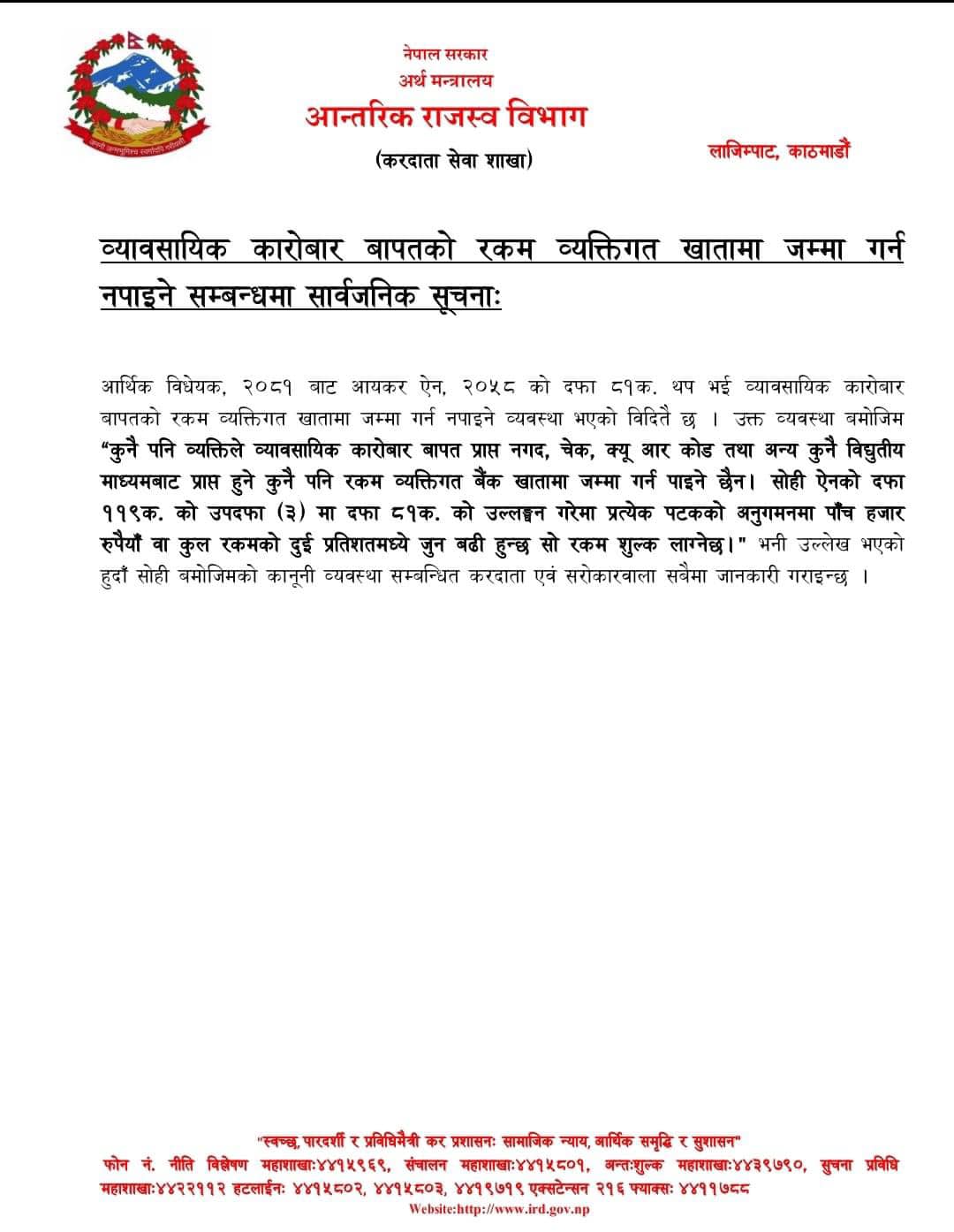

Tax Issues: Mixing personal and business funds can complicate your tax filings. The IRD may penalize you for improper reporting or attempt to audit your finances.The inland revenue department has issued a notice relating to the fines for depositing the business income into the personal account.

The inland revenue shall levy fines of Rs 5,000 per attempt or 2% of such deposited amount, whichever is higher.This means a person should not deposit the business payment received in the form of cash, QR payment, cheque and other means of electronic payment in the personal account.

Legal Compliance: Depending on your jurisdiction, there may be specific regulations regarding how businesses handle transactions. Deposit of business funds into a personal account might violate these regulations, leading to fines or legal actions.

Accounting Complications: It becomes challenging to keep accurate records of business income and expenses, which are necessary for financial reporting and tax purposes.

Financial Institution Policies: Banks and financial institutions have policies against commingling personal and business funds. Violating these policies could result in fines or closure of accounts.

To avoid these issues, it's essential to maintain separate business and personal accounts and adhere to proper accounting practices. If you're unsure about the legal and tax implications specific to your situation, consulting with a qualified accountant or business advisor is recommended.

Post your comment

⋅

0 comments

have been posted.

More Stories

Follow Us

All Rights Reserved © 2023